How to Choose a Tax Relief Company Without Getting Scammed

If you are trying to choose a tax relief company that will actually help you, you are already asking the right question.

People with IRS tax debt are often under pressure. They may be receiving notices, dealing with penalties, or worried about liens, levies, or wage garnishment. That pressure makes them vulnerable to aggressive advertising from companies promising fast results, “pennies on the dollar” settlements, or overnight tax debt relief.

That is where taxpayers need to slow down.

Not every tax relief company operates the same way. Some firms provide real IRS representation through licensed tax professionals. Others operate more like sales companies, collecting large retainers before a qualified professional ever reviews the case.

The difference is not always obvious from the outside, but it becomes clearer when you know what to look for.

Before hiring any tax relief company, you should know who holds the credentials, who will personally work on your case, how the fees are structured, and whether the firm is willing to put clear expectations in writing. A legitimate tax resolution firm should be able to explain your options without guaranteeing an outcome the IRS has not approved.

Before hiring anyone, review the Ultimate IRS Tax Debt Resolution Guide so you understand the main IRS options before a sales call frames them for you.

By the end of this article, you will have a practical framework for choosing a tax relief company with more confidence. We will cover how to verify credentials, how to review fee structures, what red flags to watch for, and which questions can help you separate a real tax advisor from a sales operation.

How to Choose a Tax Relief Company Summary TLDR;

Verify who will actually handle your case.

Look for an Enrolled Agent, CPA, or tax attorney.

Avoid firms that rely on vague titles, pressure sales, or guaranteed settlement promises.

A legitimate firm should explain fees, scope of work, risks, and realistic IRS options.

Check reviews carefully, especially complaint patterns and resolved outcomes.

The safest choice is a firm with verified credentials, transparent pricing, real experience, and honest expectations.

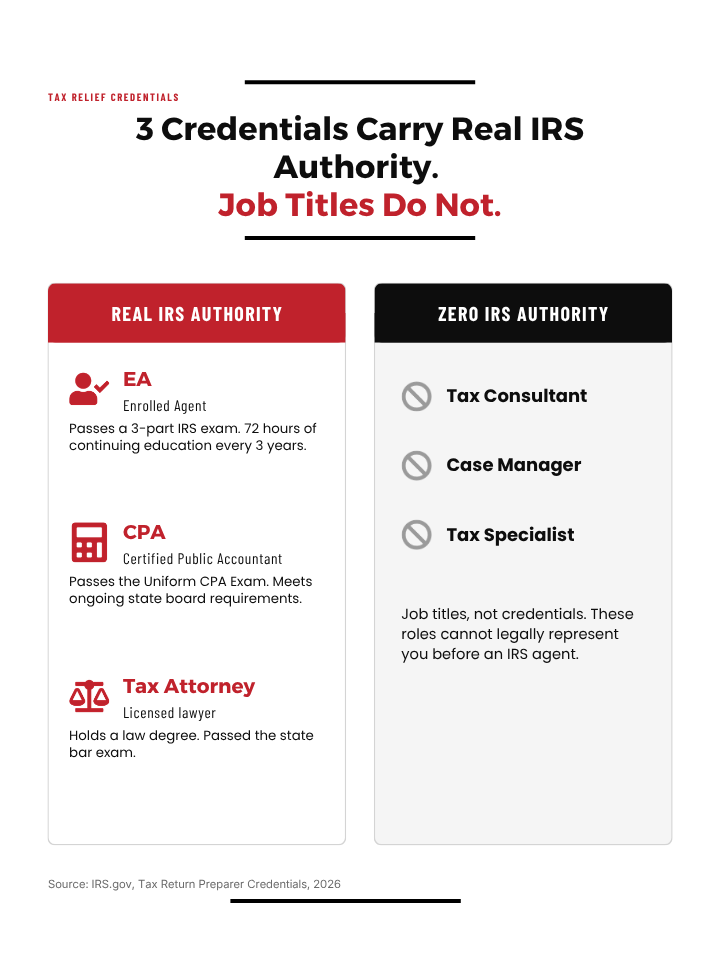

The credentials that actually matter at any tax relief firm

Only three professional designations authorize someone to represent you before the IRS without restriction: an Enrolled Agent (EA), a Certified Public Accountant (CPA), or a Tax Attorney. An EA must pass a rigorous three-part IRS examination and complete 72 hours of continuing education every three years. CPAs must clear the Uniform CPA Examination and meet ongoing state board requirements. Tax attorneys hold a law degree and passed the bar. Only these three designations carry actual IRS representation authority. For an official overview, review theIRS guide to tax return preparer credentials.

Titles like "Tax Consultant," "Case Manager," or "Tax Specialist" carry zero IRS representation authority. These titles often indicate non-licensed staff who cannot legally represent you before an IRS agent. This is one of the most common ways mills operate: a credentialed professional signs off on the firm's marketing, while unlicensed staff handle the actual casework. Always verify who is doing what before you sign anything. Form 2848 vs Form 8821 matters because one gives representation authority, while the other generally gives information access only.

IRS Form 2848 Power of Attorney is the document that allows a qualified representative to speak directly with the IRS for you.

For serious IRS issues, including Offer in Compromise submissions, audit representation, liens, and levies, the strongest representation combines legal expertise with direct IRS practice authority. A J.D. plus Enrolled Agent credential structure means one credentialed professional navigates both legal strategy and IRS procedure on your case, rather than handing off your file to support staff once the retainer clears. If a company recommends settlement, compare that pitch against how the IRS Offer in Compromise program actually works.

Always ask for the name and credential number of the person personally working your file. Then verify it. For Enrolled Agents, email epp@irs.gov with the agent's name and EA number. You can alsoverify the status of an enrolled agent through the IRS directory. For CPAs and tax attorneys, use your state's licensing board. Professional memberships in the National Association of Enrolled Agents (NAEA) or the American Institute of CPAs (AICPA) are secondary signals of ethical commitment, but direct credential verification is non-negotiable.

Why credential verification protects you

Credential verification isn't just due diligence, it's your clearest protection against mills that front one licensed professional in marketing while routing cases to unlicensed staff. A firm that resists this step is answering your most important question before you've even asked it.

How to read fee structures and what fair pricing looks like

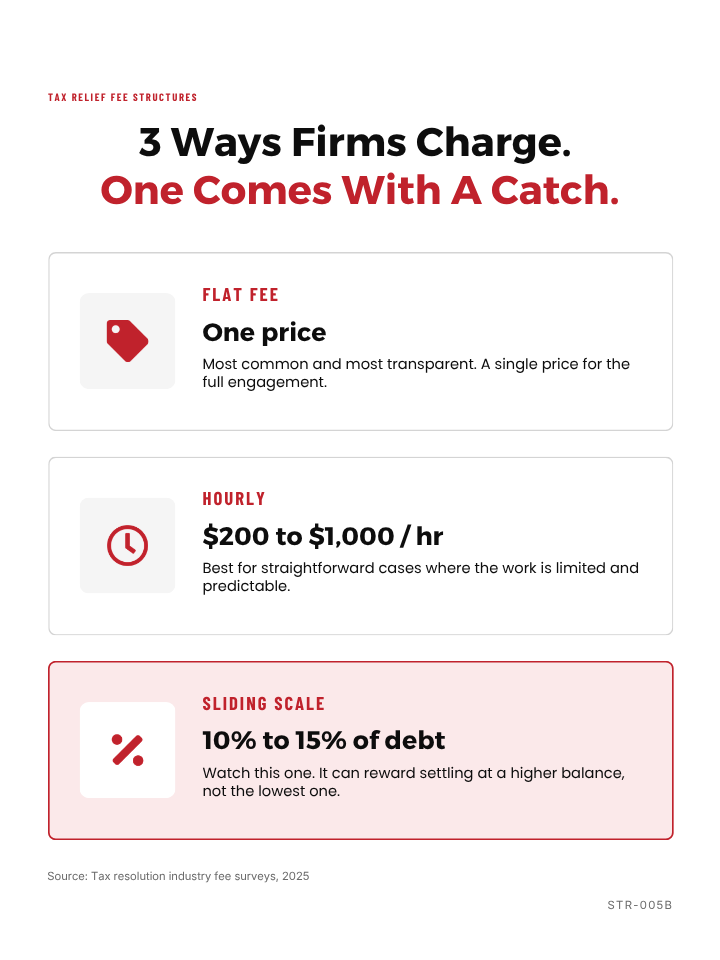

Tax settlement companies typically use one of three pricing models: flat fees (most common and most transparent), hourly rates ranging from $200 to $1,000 per hour (best for straightforward cases), and sliding scale fees of 10 to 15 percent of the total debt. Be cautious with sliding scale arrangements, as they can create an incentive to settle cases at the highest possible balance rather than the lowest.

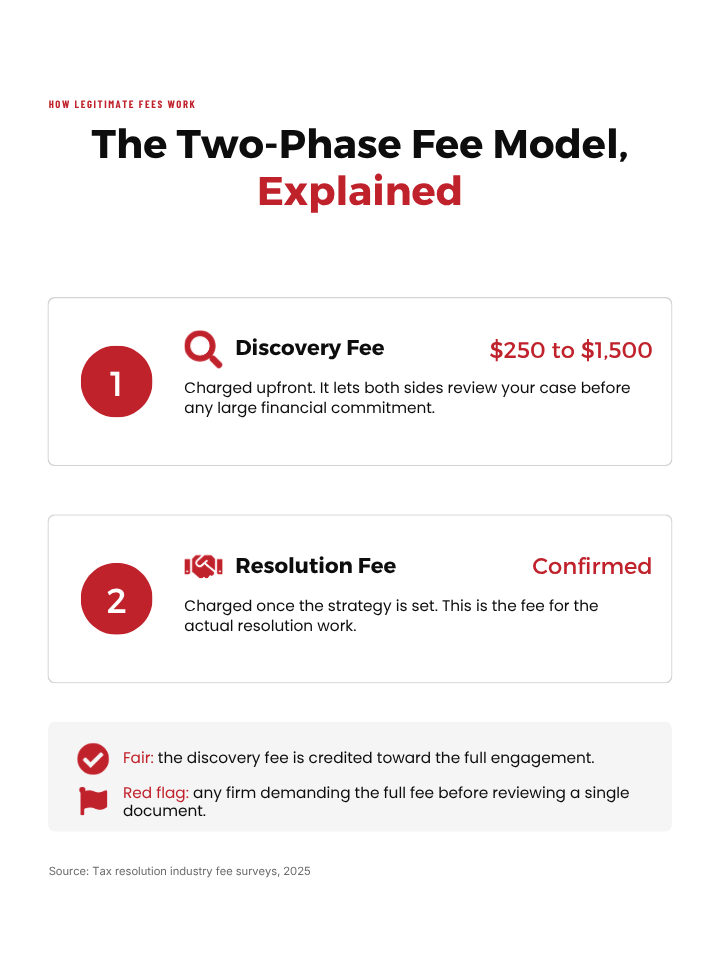

Many legitimate firms use a two-phase model: a discovery or investigation fee of $250 to $1,500 upfront, followed by resolution fees once the strategy is confirmed. This structure is legitimate when the discovery fee is credited toward the full engagement, it gives both parties a chance to assess the case before a large financial commitment. The red flag is any firm demanding the full resolution fee before reviewing a single document.

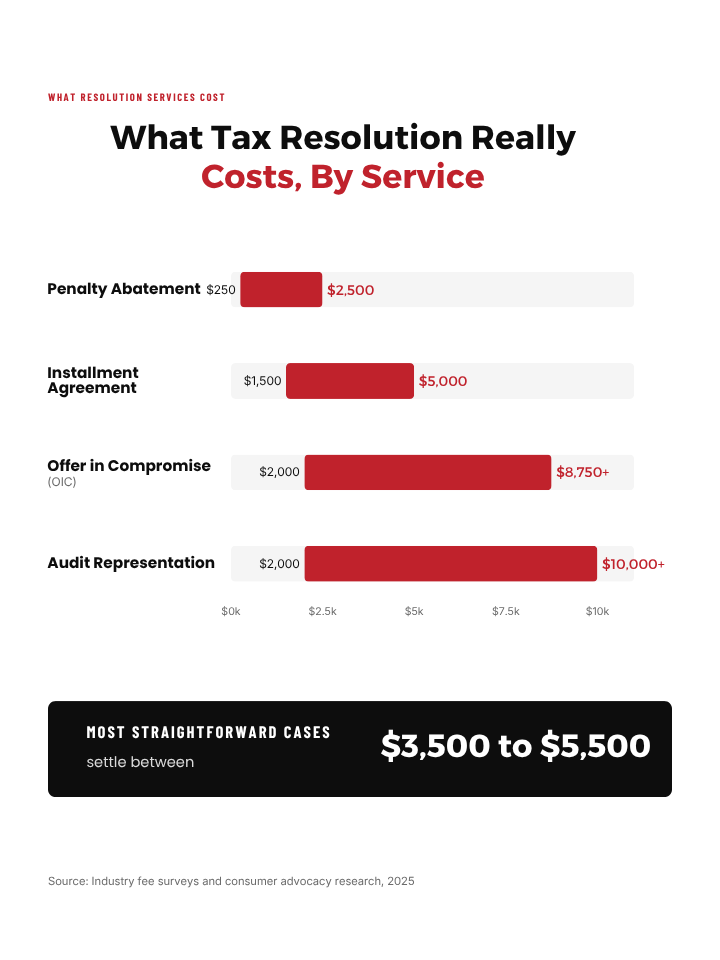

Realistic price ranges by service type, based on industry surveys and consumer advocacy research, look like this:

| Service type | Realistic price range |

|---|---|

| Installment agreements | $1,500 to $5,000 depending on debt size |

| Offer in Compromise | $2,000 to $8,750+ depending on complexity |

| Penalty abatement | $250 to $2,500, often bundled with other services |

| Audit representation | $2,000 to $10,000+ |

Most straightforward resolution cases settle between $3,500 and $5,500 in professional fees. The question isn't just "how much?" It's "what exactly does this fee cover, and what happens if the IRS rejects the first approach?" A legitimate firm answers that question directly. If appeals or refiling require a new retainer, a practice that has generated significant consumer complaints, you need to know that before you sign anything. For practical tactics and alternatives, consider our 5 ways to get rid of IRS Tax Debt guide.

Red flags that separate credible firms from the mills

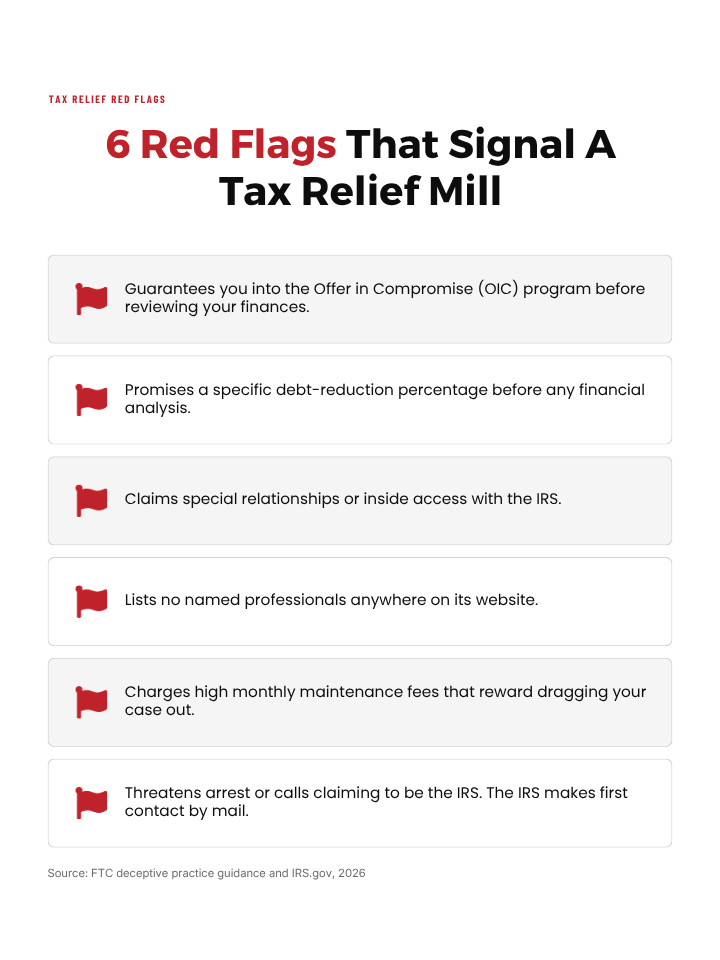

Any firm that guarantees acceptance into the Offer in Compromise program before reviewing your finances is lying to you. Only the IRS decides whether an offer is accepted. Specific percentage debt reductions promised before a financial analysis, claims of "special IRS relationships," and guarantees that your offer will never be denied are all FTC-flagged deceptive practices. Legitimate tax attorneys and enrolled agents give you a range of realistic outcomes after reviewing your actual financials, not a sales number designed to get you to sign.

Structural warning signs are just as important as specific promises. Watch for firms with no named professionals on their website, heavy TV or radio advertising with no local presence, and high monthly "maintenance fees" that give the firm a financial incentive to drag out your case rather than resolve it. Unsolicited calls or letters using official-sounding agency names, urgent "limited time" language, and any threat of arrest are textbook scam signatures. The IRS makes first contact by mail, not by phone.

Refusing to disclose who will specifically handle your file is a disqualifying red flag on its own, and it's a structural problem, not just a transparency issue. When you don't know who's working your case, you have no way to verify their credentials, evaluate their experience, or hold them accountable if the work goes sideways. If a firm won't give you a name and a license type, walk away.

If you encounter a fraudulent tax relief company, you have three reporting channels. File a referral using the IRS Form 14242 Document Upload Tool at theIRS Document Upload Tool (Form 14242), or fax a completed form to 877-477-9135. Report government impersonation or identity theft tactics to the FTC at ReportFraud.ftc.gov. For debt management complaints, contact your state attorney general's consumer protection division.

How to verify a tax relief company's reputation before hiring

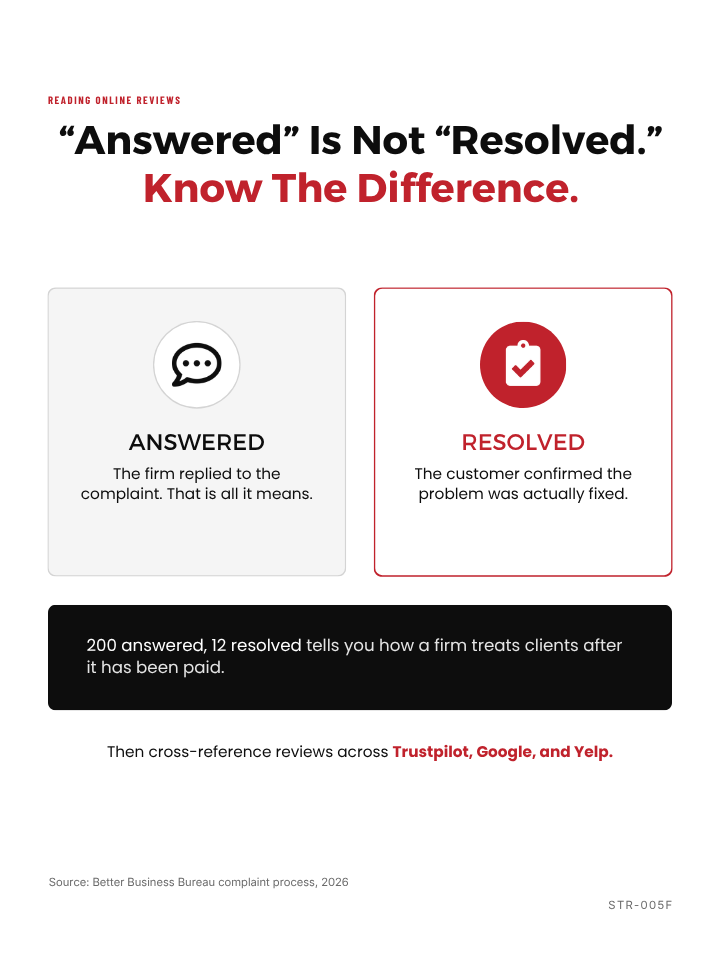

BBB accreditation and a letter grade are a starting point, not a finish line. The distinction that actually matters is between "Answered" complaints and "Resolved" complaints. An answered complaint means the firm responded. A resolved complaint means the customer confirmed the problem was fixed. A firm with 200 answered complaints and 12 resolved ones is telling you something important about how it treats clients after taking their money. Learn more about the BBB complaint process.

Cross-reference tax relief company reviews across Trustpilot, Google, and Yelp. Trustpilot uses a reviewer verification system that adds a layer of accountability not present on platforms that allow fully anonymous posts, though no review platform is entirely fraud-proof. Search the FTC's action database and your state attorney general's consumer protection division for any formal regulatory actions against the firm. Ask whether the company has had data security breaches; you're handing over financial documents, tax returns, and Social Security numbers, and that data deserves real protection.

Legitimate tax debt relief companies can point to specific case outcomes, not just testimonials with first names only. Ask for anonymized examples of accepted Offers in Compromise or resolved audit cases with approximate figures. A firm doing real work can share that information. One that can't likely doesn't have results worth sharing.

Five questions to ask in your first consultation

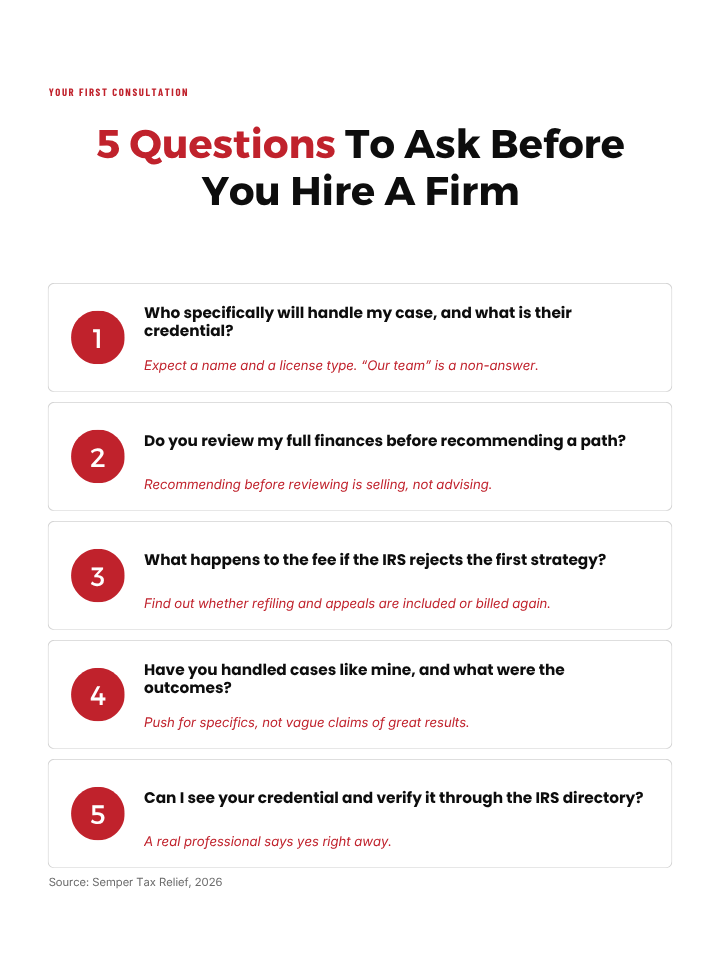

Your consultation is an interview, not a sales call. The answers you get in the first 20 minutes tell you most of what you need to know about how the firm actually operates.

1. Who specifically will handle my case, and what is their credential?

Expect a name and a license type, not a job title. If the answer is "our team," that's a non-answer.

2. Do you review my full financial picture before recommending a resolution path?

Any firm recommending an OIC or installment agreement before seeing your financials is selling, not advising.

3. What is your fee structure, and what happens if the IRS rejects the initial strategy?

Find out whether re-filing or appeals are included in the original fee or billed separately.

4. Have you handled cases similar to mine, and what were the outcomes?

Push for specifics, not vague claims of great results.

5. Can I see your credential and verify it through the IRS directory?

A credentialed professional says yes immediately and gives you the information you need to verify.

Direct answers, a willingness to show credentials, and honest timelines signal a legitimate firm. Pressure to sign a retainer before the consultation ends, "proprietary process" language that avoids transparency, and vague answers to direct questions are all forms of deflection. You deserve clear answers before you spend anything. A serious case review should start with tax relief supporting documents because the IRS reviews proof, not promises.

What realistic outcomes look like from a legitimate tax resolution firm

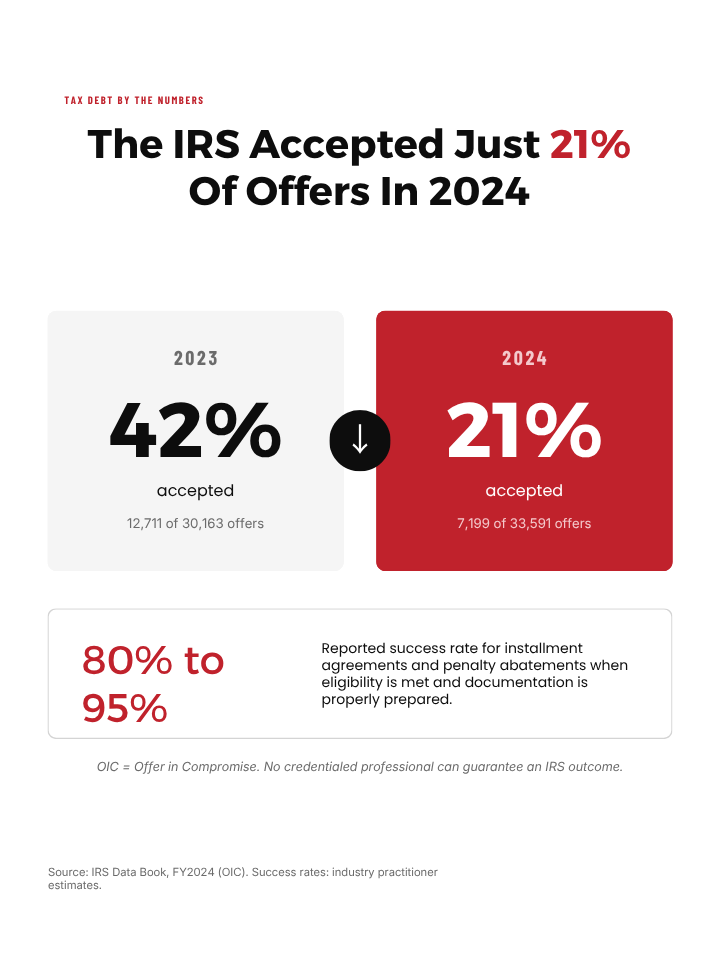

According to IRS Data Book statistics, the IRS accepted roughly 40 percent of Offer in Compromise applications in 2023. That rate dropped to approximately 21 percent in 2024. Most applicants who file on their own don't qualify or file incorrectly, submitting offers that don't align with the IRS's Reasonable Collection Potential calculation. Some specialized OIC firms report acceptance rates near 95 percent for the cases they actually submit, a figure that reflects rigorous pre-qualification rather than any special standing with the IRS. A legitimate firm only submits an OIC when the financial analysis shows the taxpayer meets the IRS threshold. They don't file and hope.

Before believing a settlement estimate, use the IRS Offer in Compromise Calculator to see whether income, expenses, and assets may support a reduced offer.

Installment agreements and penalty abatements carry 80 to 95 percent success rates when eligibility criteria are met and documentation is properly prepared. If penalties make up a large part of the balance, IRS penalty forgiveness may be reviewed before choosing a full tax settlement strategy.

These outcomes aren't guaranteed either, but the odds improve substantially when the person filing understands the IRS's requirements and has handled similar cases before. If you can afford monthly payments, IRS payment plans may be more practical than paying a firm to force an OIC that does not fit.

No credentialed professional can guarantee a specific outcome. The IRS makes the final call, full stop. Any firm that says otherwise is not being straight with you. What you're paying for is credentialed preparation, strategic positioning, and direct IRS representation, the factors that move your odds from 21 percent to 95 percent when your case is properly qualified and filed.

How to Choose a Tax Relief Company Without Getting Scammed FAQs

-

A tax relief company should have licensed professionals who are legally authorized to represent taxpayers before the IRS. The main credentials to look for are Enrolled Agent, CPA, or tax attorney. Titles like “tax consultant,” “case manager,” or “tax specialist” are not enough by themselves. Before hiring anyone, ask who will personally handle your case and verify their credential.

-

A legitimate tax relief company should clearly identify the licensed professional assigned to your case, explain your options after reviewing your financial situation, provide a written fee agreement, and avoid guaranteed promises. The firm should be willing to discuss realistic outcomes, possible risks, timelines, and what happens if the IRS rejects the first strategy.

-

Major red flags include guaranteed “pennies on the dollar” promises, pressure to sign immediately, vague pricing, no named licensed professional, claims of special IRS relationships, and large upfront fees before any case review. If a company recommends an Offer in Compromise before reviewing your income, expenses, assets, and filing compliance, that is a warning sign.

-

No. No tax relief company can guarantee that the IRS will settle your tax debt before reviewing your financial records. The IRS decides whether an Offer in Compromise, payment plan, penalty relief, or hardship status will be approved. A trustworthy firm can explain what may be possible, but it should not promise a specific IRS outcome before doing the work.

-

A tax relief company should review your IRS notices, tax years owed, filing compliance, income, expenses, assets, liabilities, and collection status before quoting a full resolution fee. If there is a levy, lien, unfiled return, payroll tax issue, or prior rejected offer, that should also be reviewed. Pricing should match the actual work required, not a generic sales package.

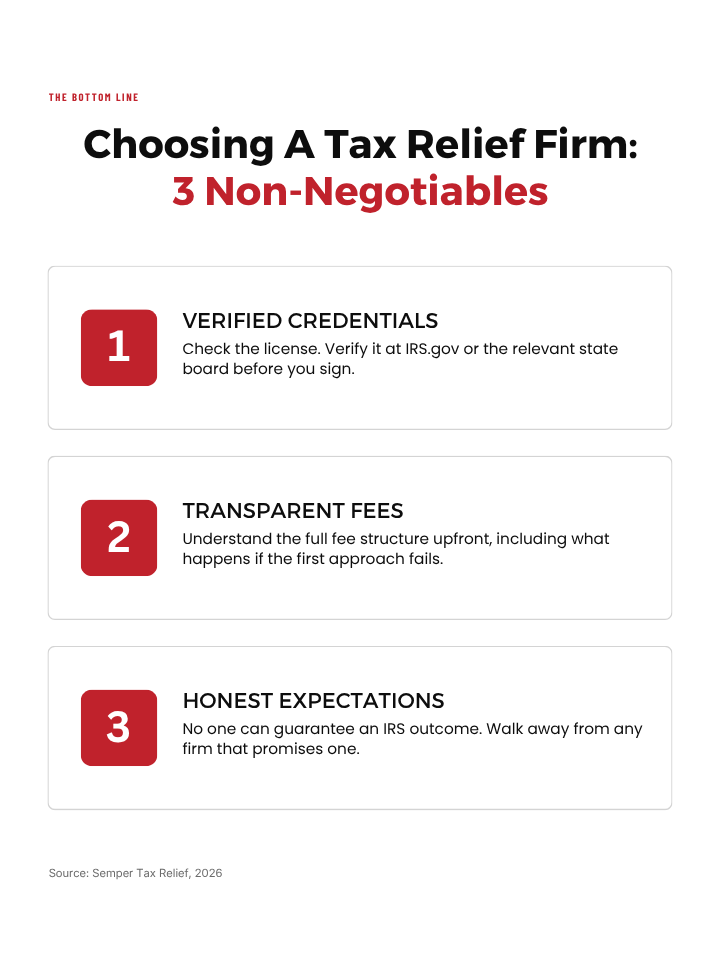

The bottom line on how to choose a tax relief company

Knowing how to choose a tax relief company comes down to three non-negotiables: verified credentials, transparent fees, and honest expectations. Run through that checklist on every firm you consider. Check the credential. Verify it at IRS.gov or with the relevant licensing board. Confirm who specifically handles your file. Understand the full fee structure before signing. Push back hard on any promise that sounds too clean, because no one can guarantee an IRS outcome.

The difference between a legitimate tax resolution firm and a mill isn't price, it's accountability. Named professionals, verifiable outcomes, and a clear picture of what's possible before you commit to anything are the markers of a firm worth trusting. Mills rely on the complexity of the IRS system to obscure what they're actually delivering, which is often nothing. For a deeper walkthrough of resolution options and how the process typically unfolds, read ourComprehensive Guide to Resolving IRS Tax Debt.

You can also review the New Client Onboarding Documents to see what a legitimate IRS representation process asks for before work begins.

If you're evaluating your options right now, Semper Tax Relief offers a no-cost case review so you can understand exactly where you stand before spending a dollar. A credentialed professional reviews your situation and gives you an honest assessment of your realistic options, no pressure, no pitch, just a clear answer. You can also review the6 Steps to IRS Tax Debt Relief to prepare for that conversation. Book online or call 24/7 to get started.