IRS Bank Levy Release

If the IRS has frozen your bank account, you need to act quickly.

A bank levy can leave you without access to money you were counting on for rent, payroll, groceries, mortgage payments, or basic living expenses

An IRS bank levy does not always mean the money is gone immediately.

In many cases, the bank must hold the funds for 21 days before sending them to the IRS. That hold period can create a short window to review your options, contact the IRS, and determine whether a levy release request may be available.

Do I Qualify for the Best Tax Relief? Find out with a Free Case Review

Call or Book Online (24 Hours /7 Days a week)

✔ 100% Confidential ✔No Sales Pressure ✔Personalized Strategy

IRS Bank Levy Release Help Before the Bank Sends the Money

What an IRS bank levy means

An IRS bank levy is a legal seizure of money in your bank account. When the IRS sends a levy to your bank, the bank may freeze the funds available in the account at the time the levy is received.

This can affect personal accounts, business accounts, savings accounts, and other bank funds. For a small business owner, a bank levy can interfere with payroll, vendor payments, rent, inventory, and operating expenses. For a family or homeowner, it can interfere with bills, food, mortgage payments, and basic household needs.

Why the bank may freeze the funds

The bank freezes the money because it has received a levy from the IRS. The bank does not decide whether the tax is correct. The bank is usually following the levy instructions.

That is why it is important to look at the IRS side of the issue quickly. The key questions are often whether the IRS followed the proper collection process, whether the taxpayer is in filing compliance, whether the levy is creating financial hardship, and whether another tax relief option may resolve the account.

Why timing matters

Timing matters because a bank levy often involves a 21 day hold. During that period, the money may be frozen, but it has not always been sent to the IRS yet.

This is the time to review the notices, confirm the tax years involved, gather financial information, and contact the IRS if a release request may be appropriate. Waiting too long can make the situation harder because the bank may send the funds to the IRS after the hold period ends.

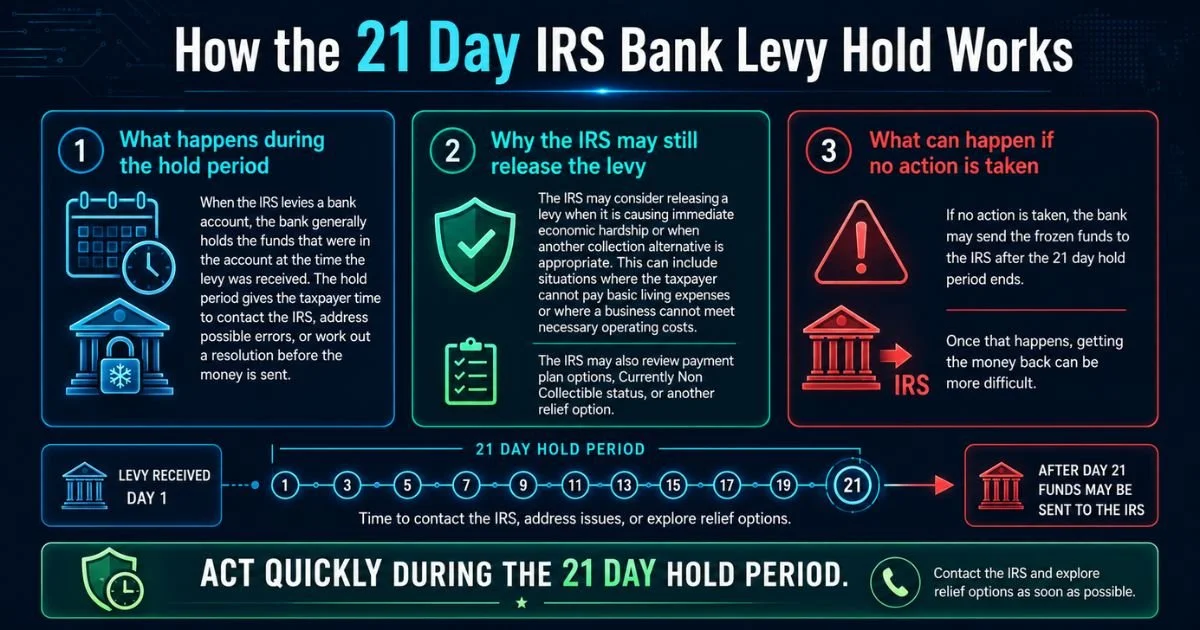

How the 21 Day IRS Bank Levy Hold Works

What happens during the hold period

When the IRS levies a bank account, the bank generally holds the funds that were in the account at the time the levy was received. The hold period gives the taxpayer time to contact the IRS, address possible errors, or work out a resolution before the money is sent.

This does not mean every levy will be released. It means there may be time to review the situation and request help if the facts support it.

Why the IRS may still release the levy

The IRS may consider releasing a levy when the levy is causing immediate economic hardship or when another collection alternative is appropriate. This can include situations where the taxpayer cannot pay basic living expenses or where a business cannot meet necessary operating costs.

The IRS may also review whether the taxpayer can enter into a payment plan, qualify for Currently Non Collectible status, or address the balance through another relief option.

What can happen if no action is taken

If no action is taken, the bank may send the frozen funds to the IRS after the 21 day hold period ends. Once that happens, getting the money back can be more difficult.

Even if the money has already been sent, the taxpayer may still need to resolve the underlying tax balance. A bank levy is often a sign that the IRS account needs a full review, not just a quick phone call.

How to Request an IRS Bank Levy Release

Financial hardship review

A financial hardship review looks at your income, expenses, assets, household size, and ability to pay basic living costs. If the levy prevents you from paying necessary expenses, that information may support a levy release request.

I help organize the financial picture so the IRS can see what is happening clearly. The goal is to present the facts in a complete and professional way.

Payment plan options

In some cases, an IRS payment plan may help resolve the collection issue and stop future levy action. The right payment plan depends on the amount owed, the tax years involved, filing compliance, financial ability, and IRS collection status.

A payment plan is not just about picking a monthly number. It should be based on what the IRS will accept and what the taxpayer can realistically maintain.

Currently Non Collectible status

Currently Non Collectible status may be an option when a taxpayer cannot afford to make payments after covering necessary living expenses. This status does not erase the tax debt. It may temporarily pause certain collection activity when the IRS agrees the taxpayer cannot pay at the moment.

For someone dealing with a frozen bank account, this option may be worth reviewing if the levy is creating serious financial hardship.

Appeals and collection alternatives

Some taxpayers may have appeal rights or other collection alternatives available. The best option depends on the notices received, the deadline dates, the type of levy, and the status of the IRS account.

I review the account before recommending a direction. The first step is understanding what the IRS has done and what options are still open.

Common Reasons the IRS May Levy a Bank Account

Unpaid tax balances

The IRS may issue a bank levy when a tax balance remains unpaid and the account has moved into collection status. This can involve personal income taxes, business taxes, payroll taxes, or multiple years of tax debt.

Ignored IRS notices

A bank levy often happens after the IRS has sent prior notices. Some taxpayers never saw the letters. Others moved, misplaced the notices, or hoped the issue would go away.

Once the IRS reaches levy action, the account usually needs immediate attention.

Defaulted payment plans

If an IRS payment plan defaults, the IRS may restart collection activity. This can happen when payments are missed, new tax debt is created, required returns are not filed, or estimated tax payments are not made when required.

Unfiled tax returns

Unfiled tax returns can also create levy problems. The IRS may be less willing to approve a payment plan or collection alternative if required returns are missing.

Before requesting certain forms of relief, filing compliance often needs to be reviewed.

How I Help With IRS Bank Levy Problems

Reviewing IRS transcripts

I review IRS transcripts to identify the tax years involved, balances owed, collection activity, filing status, penalties, payments, and notices issued. This helps determine what the IRS is trying to collect and what needs to be addressed.

Confirming filing compliance

The IRS often wants taxpayers to be current with required tax filings before approving certain collection options. I review whether returns are filed, whether any years are missing, and whether the account has any compliance issues that may block relief.

Preparing financial information

A levy release request often depends on financial documentation. This may include proof of income, bank statements, rent or mortgage information, utility expenses, business operating expenses, payroll costs, and other necessary bills.

I help organize the information so the IRS can review it efficiently.

Contacting the IRS for possible release

Once the facts are reviewed, I can contact the IRS to request a possible levy release or discuss available collection options. The request must match the facts of the case.

There are no guarantees with an IRS bank levy release. The goal is to act quickly, present the right information, and pursue the best available option based on your situation.

Get Help With an IRS Bank Levy

Act before the hold period ends

If your bank account has been frozen by an IRS levy, do not wait until the 21 day hold period is almost over. The sooner the account is reviewed, the more time there may be to request help.

Upload your notices and bank levy documents

To review your case, I need to see the IRS notices, bank levy paperwork, account information, and any documents showing financial hardship. These documents help confirm what the IRS is collecting and what options may be available.

Request a free case review

If you need IRS bank levy help, request a free case review with Semper Tax Relief. I will review the situation, explain what may be happening, and help you understand possible next steps.

IRS Bank Levy Release Frequently Asked Questions

-

An IRS bank levy is when the IRS sends a legal order to your bank to freeze money in your account and send it to the IRS after the required hold period. It is one of the IRS collection tools used to collect unpaid tax debt.

-

In many IRS bank levy cases, the bank holds the money for 21 days before sending it to the IRS. This hold period may give the taxpayer time to contact the IRS, review the account, and request a possible levy release if the facts support it.

-

Yes, an IRS bank levy may be released in certain situations. A release may be considered if the levy is causing immediate economic hardship, if the taxpayer enters into an acceptable resolution, or if another collection alternative applies. Each case depends on the facts.

-

If the bank already sent the money to the IRS, options may be more limited, but the account should still be reviewed. In some cases, a taxpayer may be able to request that levy proceeds be returned. Even if that is not available, the underlying tax issue still needs to be resolved to help prevent future collection action.

-

Financial hardship may help support a request for an IRS levy release. The IRS will usually want to review income, expenses, assets, household needs, and ability to pay. If the levy prevents you from paying necessary living expenses, that information should be documented clearly.