Trust Fund Recovery Penalty Help

When a business falls behind on payroll taxes, the IRS may look beyond the business itself. In some cases, the IRS may try to hold an owner, officer, manager, or other responsible person personally liable for certain unpaid payroll taxes. This is called the Trust Fund Recovery Penalty.

If the IRS is contacting you about payroll tax personal liability, this is not something to answer casually. The facts matter. Your role matters. Your authority matters. The timing of your decisions matters. Before speaking with the IRS, it is important to understand what they are trying to prove and how your answers may affect the case.

Trust Fund Recovery Penalty Help for Payroll Tax Problems

Payroll tax debt is one of the most serious business tax problems because the IRS views withheld payroll taxes differently than ordinary business debt. These taxes are withheld from employees’ wages and are supposed to be sent to the IRS.

When those funds are not paid, the IRS may investigate who had control over payroll, money decisions, tax deposits, bank accounts, and vendor payments.

What the Trust Fund Recovery Penalty means

The Trust Fund Recovery Penalty is a personal assessment the IRS may make against someone it believes was responsible for collecting, accounting for, or paying payroll taxes, and who willfully failed to make sure those taxes were paid.

This does not always mean the person stole money or acted with bad intent. In many cases, the issue is whether the person had authority and knew, or should have known, that payroll taxes were not being paid while other bills were being paid.

Why the IRS may assess it personally

The IRS may assess the Trust Fund Recovery Penalty personally when the business owes certain unpaid payroll taxes and the IRS believes one or more people inside the business were responsible for the unpaid trust fund portion.

This can include business owners, officers, payroll decision makers, or others with authority over financial decisions.

If assessed, the IRS can try to collect from the individual, not just the business. That means the issue can follow you even if the business closes, changes ownership, or can no longer pay.

Why business owners and responsible parties should take it seriously

A Trust Fund Recovery Penalty case is not just about the business balance. It can become a personal collection case. You may be dealing with IRS notices, contact from a Revenue Officer, a request for an interview, or a proposed assessment letter. You may also be trying to keep the business operating while handling vendors, employees, payroll, and tax compliance.

I help clients slow the process down, organize the facts, review the risk, and respond in a way that protects their rights.

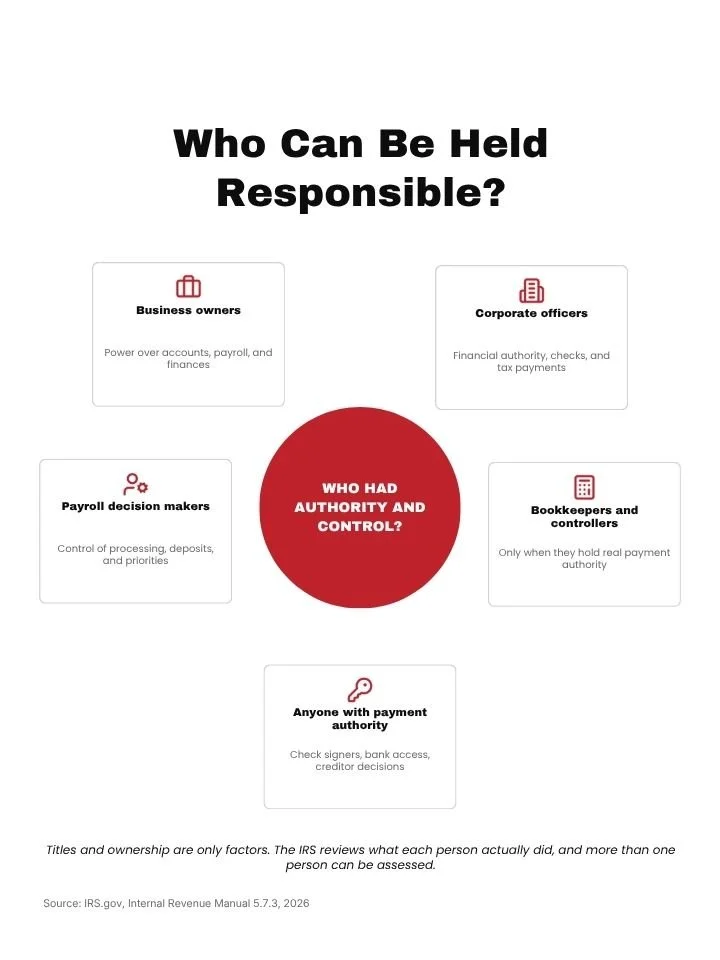

Who Can Be Held Responsible

The IRS does not limit Trust Fund Recovery Penalty investigations to the person whose name is on the business. The IRS looks at who had actual authority and control.

Business owners

Business owners are often reviewed because they may have authority over bank accounts, payroll decisions, tax deposits, and company finances.

Ownership alone does not answer every question, but it is an important factor. The IRS will usually look at whether the owner had the power to decide which bills were paid and whether payroll taxes were knowingly left unpaid.

Corporate officers

Corporate officers may be reviewed if they had financial authority, signed checks, directed payroll, handled tax payments, or had control over business funds.

A title by itself does not always prove responsibility. The IRS looks at what the person actually did inside the business.

Payroll decision makers

A person involved in payroll decisions may face review if they controlled payroll processing, tax deposits, employee withholding, or payment priorities.

The IRS may ask who decided to pay net wages, who knew taxes were due, and who decided whether tax deposits were made.

Bookkeepers or controllers in certain cases

A bookkeeper, controller, or finance employee may be reviewed if they had meaningful authority over payments or financial decisions.

In many businesses, bookkeepers follow instructions and do not control payment decisions. In other cases, a finance employee may have more authority. The facts determine the level of risk.

Anyone with authority over tax payments

The IRS may review anyone who had the ability to direct payment of taxes or decide which creditors were paid.

This can include people who signed checks, approved electronic payments, controlled bank access, managed payroll deposits, directed accounting staff, or decided to pay vendors while payroll taxes remained unpaid.

IRS Form 4180 and the Interview Process

IRS Form 4180 is used during a Trust Fund Recovery Penalty investigation. It is an interview form where the IRS asks questions about your role, authority, knowledge, and involvement with the business.

This interview matters. Your answers can affect whether the IRS believes you are responsible and whether the IRS believes the failure to pay was willful.

What the IRS is trying to determine

The IRS is usually trying to determine two major points. First, whether you were a responsible person. Second, whether the failure to pay payroll taxes was willful.

The IRS may ask about your title, ownership, check signing authority, bank access, payroll involvement, hiring authority, bookkeeping control, tax deposit knowledge, and payment decisions.

Responsibility

Responsibility means the IRS believes you had enough authority or control to make sure payroll taxes were paid. The IRS may review whether you could sign checks, access bank accounts, authorize payments, decide which bills were paid, hire or fire employees, sign tax returns, approve payroll, or communicate with the IRS. More than one person can be considered responsible.

Willfulness

Willfulness does not always mean fraud or bad intent. In many Trust Fund Recovery Penalty cases, the IRS focuses on whether the person knew payroll taxes were unpaid and allowed other payments to be made instead.

For example, the IRS may review whether the business paid rent, vendors, lenders, contractors, or other expenses while payroll taxes were not being deposited.

Why answers matter

The Form 4180 interview is not just a conversation. It creates a record. If you answer without reviewing the facts, payroll records, bank records, business structure, and your actual authority, you may create problems that could have been avoided.

Before an interview, I help clients understand the questions, review the timeline, identify supporting documents, and prepare for the issues the IRS is likely to focus on.

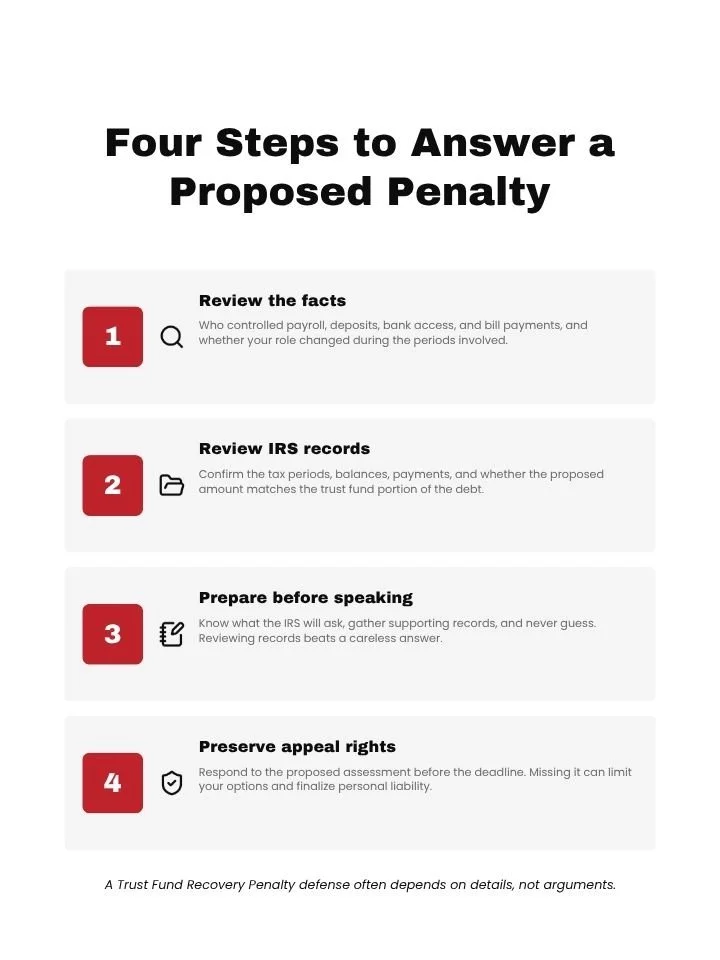

How to Respond to a Proposed Trust Fund Recovery Penalty

If the IRS proposes a Trust Fund Recovery Penalty, do not ignore the letter. The proposed assessment stage may include important appeal rights and deadlines. A careful response can make a real difference.

Review the facts

The first step is to review what actually happened. This may include who controlled payroll, who made deposits, who had access to bank accounts, who decided which bills were paid, who knew taxes were unpaid, and whether your role changed during the tax periods involved. A Trust Fund Recovery Penalty defense often depends on details.

Review IRS records

IRS records may show the payroll tax periods involved, the unpaid balances, payments made, penalties, deposits, and business compliance history.

I also review whether the IRS is focusing on the correct periods and whether the proposed amount appears to match the trust fund portion of the payroll tax debt.

Prepare before speaking with the IRS

Preparation is important before speaking with a Revenue Officer or answering Form 4180 questions. I help clients understand what the IRS is asking, what records may support their position, and how to avoid guessing. If you do not know an answer, it is better to review the records than to give a careless response.

Preserve appeal rights

If the IRS proposes the Trust Fund Recovery Penalty, you may have the right to appeal before the assessment is finalized. The deadline matters. Missing the deadline can limit your options. I help clients review proposed assessment letters, evaluate appeal arguments, and respond before rights are lost.

How I Help With Trust Fund Recovery Penalty Cases

At Semper Tax Relief, my goal is to help you understand your exposure, protect your rights, and address both the personal liability risk and the business payroll tax problem.

Reviewing the payroll tax history

I review the payroll tax periods involved, the IRS balance, payments made, missing deposits, notices issued, and the current status of the business tax account. This helps identify whether the IRS is pursuing the business, the individuals, or both.

Reviewing responsible person risk

I review your role in the business, including ownership, title, check signing authority, bank access, payroll authority, tax deposit knowledge, and payment control. This helps determine whether the IRS may try to classify you as a responsible person.

Preparing for IRS contact

If the IRS requests a Form 4180 interview, I help you prepare before the conversation takes place.

That may include reviewing records, organizing the timeline, clarifying your role, and identifying areas where the IRS may ask follow up questions.

Preparing for IRS contact

If the IRS requests a Form 4180 interview, I help you prepare before the conversation takes place. That may include reviewing records, organizing the timeline, clarifying your role, and identifying areas where the IRS may ask follow up questions.

Planning the business tax resolution

A Trust Fund Recovery Penalty case often connects to a larger business payroll tax issue.

The business may need a payroll tax resolution plan, current compliance, missing returns filed, deposits corrected, or a strategy for dealing with a Revenue Officer.

Possible options may include an installment agreement, penalty relief, appeal review, business tax debt resolution, or other IRS collection alternatives based on the facts.

If state payroll tax agencies are also involved, I can review those issues as part of the overall resolution strategy.

Get Help Before Personal Liability Is Assessed

The best time to get help is before the IRS finalizes personal liability.

Once the Trust Fund Recovery Penalty is assessed, the IRS may pursue collection against the individual. That can include notices, payment demands, liens, levies, or other collection action depending on the case.

Do not ignore Form 4180

If the IRS asks you to complete Form 4180 or attend an interview, take it seriously. This is where the IRS builds the record for responsibility and willfulness. You should understand the process before answering.

Review your exposure

You may not know whether you are at risk until the facts are reviewed. Your title may not tell the whole story. Your ownership percentage may not tell the whole story. Your actual authority, knowledge, and involvement are what matter.

Request a free case review

If you received an IRS Form 4180 request, a proposed Trust Fund Recovery Penalty letter, or contact from a Revenue Officer about payroll taxes, I can review your situation and explain your options.

Request a free case review with Semper Tax Relief. I will help you understand what the IRS is reviewing, what your next step should be, and how to protect your rights.

Get Trust Fund Recovery Penalty Help Today

If the IRS is investigating you for payroll tax personal liability, do not wait until the assessment is final. I can help you review the payroll tax history, prepare for IRS contact, evaluate your personal risk, and respond to the IRS with a clear strategy.

Request a free case review today with Semper Tax Relief.

Frequently Asked Questions About Trust Fund Recovery Penalty Help

-

The Trust Fund Recovery Penalty is a personal IRS assessment for certain unpaid payroll taxes. It may apply when the IRS believes a person was responsible for collecting or paying payroll taxes and willfully failed to make sure those taxes were paid.

-

The IRS may review business owners, corporate officers, payroll decision makers, controllers, bookkeepers, or anyone with authority over tax payments. More than one person can be held responsible if the IRS believes multiple people had control and knowledge.

-

IRS Form 4180 is an interview form used during a Trust Fund Recovery Penalty investigation. The IRS uses it to ask about your role, authority, knowledge of unpaid payroll taxes, and involvement in business payment decisions.

-

Yes, you may have appeal rights if the IRS proposes a Trust Fund Recovery Penalty. The deadline in the IRS letter is important. If you receive a proposed assessment letter, review it right away so you do not miss the opportunity to respond.

-

Yes, if the IRS assesses the Trust Fund Recovery Penalty against you, it can try to collect the assessed amount from you personally. That is why it is important to respond carefully during the investigation stage and review your options before the assessment becomes final.