IRS Federal Tax Lien Help

An IRS federal tax lien can affect your property, your business, and your ability to complete an important financial transaction. It also means the IRS has moved beyond sending ordinary balance due notices and has taken action to protect its claim against your property.

I help taxpayers understand what the IRS filed, protect available appeal rights, and address the tax debt that caused the lien. Whether your balance involves one tax year, prior tax years, or several years of IRS debt, I begin by reviewing the entire account before recommending a resolution strategy.

What Is an IRS Federal Tax Lien?

A federal tax lien is the government’s legal claim against your property when the IRS has assessed a tax, sent a demand for payment, and the balance remains unpaid.

The lien can attach to property and rights to property you currently own. It may also affect certain property you acquire while the lien remains enforceable.

A Notice of Federal Tax Lien is the document the IRS files in the public record to notify creditors and other interested parties that the government has a claim against your property.

The filing may involve individual income taxes, business income taxes, payroll taxes, penalties, interest, or balances from several tax years.

What a Notice of Federal Tax Lien Can Affect

A Notice of Federal Tax Lien can create problems when you are trying to sell or refinance a home, transfer property, obtain business financing, or resolve competing claims from other creditors.

The notice does not mean the IRS immediately owns your property. It means the government has formally recorded its legal interest.

The effect on a particular transaction depends on the type of property, available equity, other recorded liens, and the amount of IRS debt.

Federal Tax Lien Versus IRS Levy H3

A federal tax lien and an IRS levy are different collection actions.

A lien is a legal claim against your property. A levy is an actual seizure of money, income, or property.

An IRS levy may reach a bank account, wages, accounts receivable, or other assets after the required collection procedures have been followed.

A taxpayer may have a filed Notice of Federal Tax Lien without an active levy. However, unresolved tax debt can continue through the IRS collection process

IRS Notices Connected to Federal Tax Liens and Collection Appeals

The IRS notice you received matters because different letters provide different rights and deadlines.

I review the notice number, notice date, response deadline, tax periods, amount listed, and the IRS office handling the account.

This helps determine whether an appeal is available and what action should be considered next.

Letter 3172 and the Notice of Federal Tax Lien

Letter 3172 is commonly used to notify a taxpayer that the IRS filed a Notice of Federal Tax Lien.

The letter also explains the right to request a Collection Due Process hearing. A taxpayer generally has 30 days to request the hearing using Form 12153.

The exact deadline printed on the notice should be reviewed immediately. A timely hearing request may allow the taxpayer to challenge whether the lien filing was appropriate and propose a collection alternative.

If the deadline has already passed, an Equivalent Hearing may still be available in some cases. However, an Equivalent Hearing does not provide all the same rights as a timely Collection Due Process hearing.

IRS LT11 Notice and Letter 1058 H3

The LT11 Notice and Letter 1058 are generally final notices of intent to levy. They are not the Notice of Federal Tax Lien itself.

These notices usually tell the taxpayer that the IRS intends to take levy action and that the taxpayer has the right to request a Collection Due Process hearing.

A taxpayer can receive a lien notice and a levy notice during the same collection case. When that happens, I review each notice separately so that an appeal deadline or available resolution option is not overlooked.

How I Help With an IRS Federal Tax Lien

My first objective is to understand the entire IRS collection case, not simply the amount printed on one notice.

A federal tax lien is usually connected to a larger tax debt problem that must be addressed before the lien can be fully resolved.

I obtain the appropriate IRS authorization, review account transcripts, identify the tax periods involved, confirm whether required tax returns have been filed, and determine which IRS collection division is handling the account.

I then evaluate appeal rights, collection deadlines, income, necessary living expenses, property equity, business activity, and the taxpayer’s ability to pay.

Reviewing Every Tax Year and Tax Period

A Notice of Federal Tax Lien may list one tax year, several prior years, or multiple types of federal tax debt.

A business lien may include income tax, payroll tax, civil penalties, or other business liabilities.

I compare the lien notice with IRS account transcripts to verify the assessed tax, payments, credits, penalties, interest, and collection status for each period.

I also look for missing returns, substitute returns prepared by the IRS, pending adjustments, audit assessments, and payments that may not have been applied correctly.

Representing You Before the IRS

As an Enrolled Agent, I am authorized to represent taxpayers before the IRS.

I communicate with the IRS concerning the lien, the underlying balance, available appeal procedures, and possible collection alternatives.

Depending on the case, this may involve the Automated Collection System, the Centralized Lien Operation, an IRS Revenue Officer, the Independent Office of Appeals, or another IRS unit.

Representation can help create a clear point of contact and reduce the risk of providing incomplete or inconsistent information to different IRS employees.

Filing an Appeal of an IRS Federal Tax Lien

A lien appeal may be appropriate when the IRS did not follow required procedures, the tax was already paid, the balance is incorrect, the lien was filed prematurely, or another collection alternative should be considered.

During a Collection Due Process hearing, a taxpayer may be able to propose an installment agreement, an Offer in Compromise, Currently Not Collectible status, or another appropriate resolution. In limited situations, the underlying tax liability may also be disputed.

An appeal does not automatically mean the IRS will remove the lien. The facts, deadlines, prior opportunities to dispute the tax, and proposed resolution all matter.

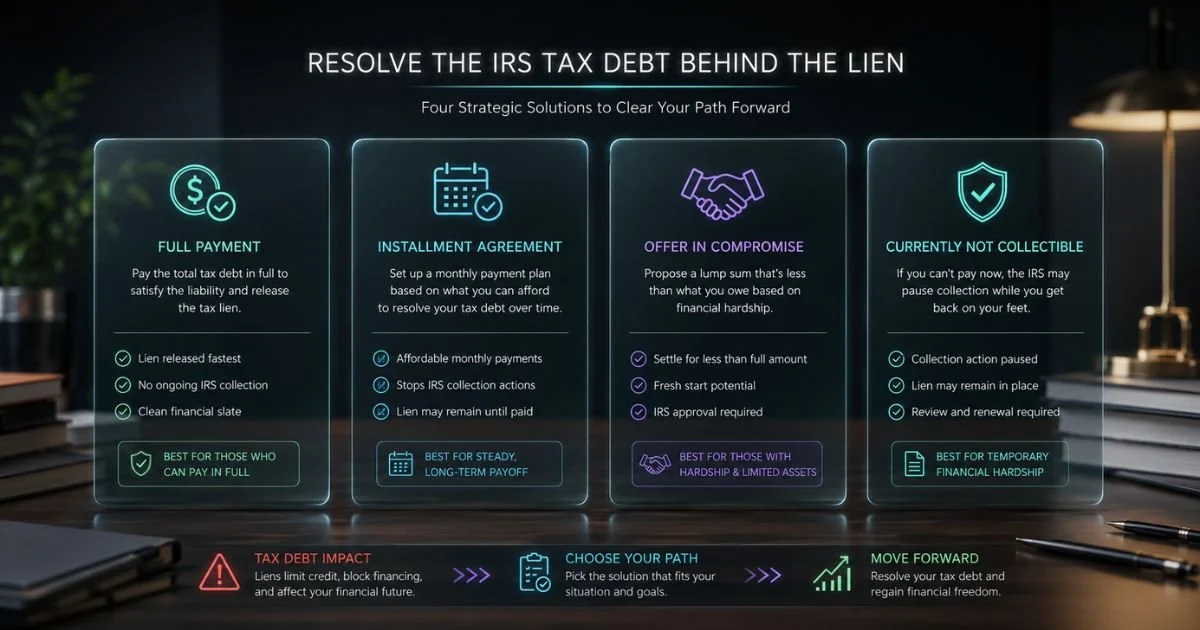

Resolving the IRS Tax Debt Behind the Lien

A Notice of Federal Tax Lien is usually not resolved by addressing the recorded document alone.

The underlying federal tax debt must also be corrected, paid, settled, or placed into an appropriate collection status.

The right option depends on the amount owed, income, expenses, asset equity, remaining collection time, filing compliance, payment compliance, and whether the taxpayer is an individual or business.

Full Payment or a Short Payment Period

Paying the tax debt in full is the most direct way to obtain a federal tax lien release.

The IRS generally releases the lien within 30 days after the tax debt is fully paid.

When full payment is possible, I verify the current payoff amount and confirm which tax periods are covered.

IRS Installment Agreement

An installment agreement allows an eligible taxpayer to pay the IRS over time.

Depending on the balance and financial condition, the arrangement may be a standard payment plan, a financially verified agreement, or a partial payment installment agreement.

Entering an installment agreement does not automatically release an existing Notice of Federal Tax Lien.

Certain qualifying taxpayers using a direct debit installment agreement may be able to request withdrawal of the notice when the IRS requirements are met.

IRS Offer in Compromise

An Offer in Compromise may allow a qualifying taxpayer to resolve federal tax debt for less than the full balance.

The IRS reviews income, necessary expenses, asset equity, ability to pay, and other relevant circumstances.

An offer is not available or appropriate for every taxpayer. Required tax returns generally must be filed, estimated tax payments must be current, and business owners with employees must meet applicable federal tax deposit requirements.

An accepted offer does not cause an immediate lien release. The IRS generally releases the lien after the accepted offer terms have been fully satisfied.

Currently Not Collectible Status

Currently Not Collectible status may be available when paying the IRS would prevent a taxpayer from meeting necessary living expenses.

The IRS may request financial statements and documents concerning income, expenses, bank accounts, and property.

This status can temporarily suspend most active collection activity, but it does not erase the tax debt.

Penalties and interest generally continue, and the IRS may still file or maintain a Notice of Federal Tax Lien.

Correcting the Balance and Requesting Penalty Relief

Some tax lien cases involve an incorrect assessment, an unprocessed return, a substitute return prepared by the IRS, a payment posting problem, an audit issue, or penalties that may qualify for relief.

I review whether the balance should be corrected before negotiating a collection resolution.

Penalty abatement may reduce the total amount owed when the taxpayer meets the applicable requirements. It does not automatically remove a federal tax lien.

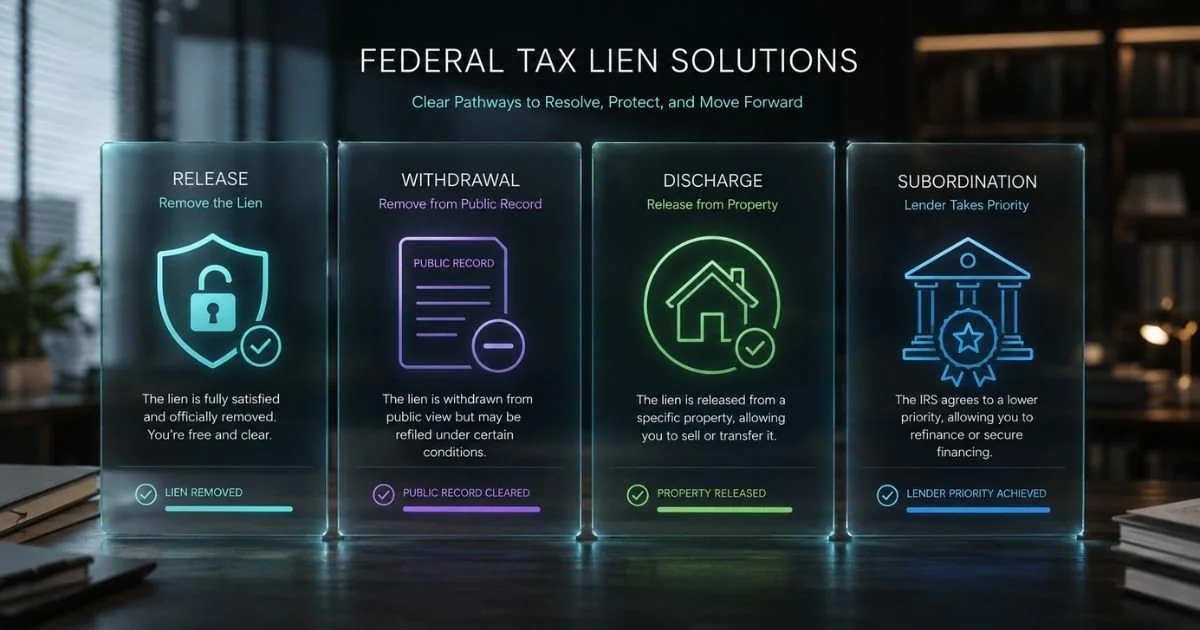

Federal Tax Lien Release, Withdrawal, Discharge, and Subordination

Federal Tax Lien Release

A lien release generally ends the federal tax lien after the liability has been fully satisfied, has become legally unenforceable, or another condition for release has been met.

A release is different from a withdrawal. A release confirms that the lien is no longer effective. It does not necessarily treat the original public notice as though it was never filed.

Withdrawal of a Notice of Federal Tax Lien

A withdrawal removes the public Notice of Federal Tax Lien and generally treats the notice as though it was not filed.

The underlying tax debt may still exist unless it has been paid or otherwise resolved.

Withdrawal may be considered when the notice was filed prematurely, IRS procedures were not followed, withdrawal would help collect the tax, a qualifying payment agreement is in place, or withdrawal is in the best interests of the taxpayer and the government.

Form 12277 is generally used to request withdrawal.

Discharge of Property From a Federal Tax Lien

A discharge removes a specific property from the effect of the federal tax lien.

It does not remove the lien from all other property and does not necessarily eliminate the underlying tax debt.

A discharge may be important when a taxpayer needs to sell real estate or transfer a specific asset.

The IRS reviews the value of the property, available equity, other secured claims, and the government’s interest in the transaction.

Subordination of a Federal Tax Lien

Subordination does not remove the federal tax lien.

It allows another creditor’s interest to move ahead of the IRS lien in priority.

This may help complete a refinancing or financing transaction when the transaction is expected to improve the taxpayer’s ability to pay the IRS.

Selling or Refinancing a Home With an IRS Tax Lien

A federal tax lien can complicate the sale or refinancing of a home, but it does not always prevent the transaction from moving forward. If there is enough equity, the IRS balance may be paid in whole or in part from the closing proceeds.

When the property is being sold for less than the total recorded liens, a discharge request may be considered. A subordination request may be considered in certain refinancing situations. These requests require documentation and should be addressed before the expected closing date

IRS Federal Tax Lien Help for Business Owners

A federal tax lien filed against a business can affect financing, equipment, accounts receivable, property, and future business transactions.

Payroll tax debt may also involve additional collection concerns, including Revenue Officer involvement and a possible Trust Fund Recovery Penalty investigation.

I review the business entity, tax types involved, federal tax deposit compliance, missing returns, financial statements, business assets, cash flow, and the owner’s connection to the liability.

The resolution must address both the existing debt and the business’s ability to remain compliant going forward.

Federal Tax Liens Involving One Year or Multiple Years

The IRS may file a Notice of Federal Tax Lien for one tax year, several prior years, or additional periods assessed after an earlier filing.

When multiple years are involved, I review each period separately.

One year may involve a filed return, another may involve an IRS audit, and another may involve a substitute return or missing payment.

Resolving only one year may not remove a lien that also covers other unpaid periods. The strategy should account for the entire enforceable IRS balance.

What to Expect From My IRS Tax Lien Review

I begin by reviewing your IRS notices and identifying any immediate response deadlines. I then obtain and analyze the relevant IRS transcripts, confirm filing compliance, and determine which tax periods are included in the lien.

Next, I review your income, expenses, assets, property equity, business activity, and ability to pay. I compare those facts with available appeal procedures, collection alternatives, and lien remedies.

After the review, I explain the available options, the documents that may be required, and the practical risks of each approach

Orange County and Nationwide IRS Federal Tax Lien Representation

Semper Tax Relief serves taxpayers in Orange County, including Brea, Laguna Niguel, and surrounding California communities. Because federal tax matters are administered by the IRS, I can also represent qualifying taxpayers throughout the United States.

If you also owe the California Franchise Tax Board or another state agency, I review those balances separately and coordinate the resolution strategy.

Request a Free IRS Federal Tax Lien Case Review

You do not have to determine the correct appeal, lien request, and tax debt resolution on your own. I can review the Notice of Federal Tax Lien, Letter 3172, LT11, Letter 1058, or another IRS collection notice you received. I will identify the tax periods involved, review the available deadlines, and explain which resolution options may fit your circumstances.

Every tax case is different. Results depend on the IRS records, financial facts, filing compliance, payment compliance, and applicable federal tax procedures.

IRS Federal Tax Lien Help FAQs

These questions address common searches from taxpayers who need help with a Notice of Federal Tax Lien, lien appeal, property transaction, or IRS tax debt resolution.

-

The appropriate method depends on the status of the debt and what you are trying to accomplish. Full payment may lead to a lien release. A qualifying taxpayer may request withdrawal of the Notice of Federal Tax Lien. A discharge may remove a specific property, while subordination may help another creditor move ahead of the IRS lien.

-

A Notice of Federal Tax Lien is a public document filed by the IRS to notify creditors that the government has a legal claim against a taxpayer’s property because of unpaid federal taxes. The notice may list one tax period or several periods.

-

Appeal rights may be available. Letter 3172 generally provides a deadline to request a Collection Due Process hearing using Form 12153. The taxpayer may challenge certain procedural issues, propose a collection alternative, and raise other permitted issues.

-

Review the notice date, response deadline, tax periods, and amount listed. Letter 3172 generally means the IRS filed a Notice of Federal Tax Lien and is notifying you of your hearing rights. Consider obtaining IRS transcripts and reviewing the case before submitting an appeal or payment proposal.

-

No. LT11 and Letter 1058 are generally final notices of intent to levy. They concern a proposed seizure of property or income, not the filing of the Notice of Federal Tax Lien. A taxpayer may receive a lien notice and a levy notice during the same IRS collection case.

-

Not automatically. An installment agreement can resolve how the debt will be paid, but an existing Notice of Federal Tax Lien may remain. Certain qualifying taxpayers with a direct debit installment agreement may be eligible to request withdrawal of the notice.

-

An accepted Offer in Compromise does not result in an immediate lien release. The IRS generally releases the federal tax lien after the taxpayer completes the accepted offer terms. Offer acceptance depends on eligibility and the taxpayer’s financial circumstances.

-

A sale may still be possible. The lien may be paid from available proceeds, or a discharge request may be considered when the transaction does not fully pay the IRS balance. The title, property equity, senior liens, closing documents, and government interest must be reviewed.

-

Refinancing may be possible in some cases through a lien subordination request. Subordination does not remove the IRS lien. It changes creditor priority when the IRS determines that doing so may improve collection of the tax debt.

-

Yes. A Notice of Federal Tax Lien may cover one tax year or one tax period. It may also include several years or several types of federal tax debt. The periods listed on the notice should be compared with IRS account transcripts.

-

Additional assessments or unpaid periods may lead to another Notice of Federal Tax Lien filing or an amendment to the recorded lien information. Resolving one year does not automatically resolve other unpaid periods.

-

The IRS generally releases a federal tax lien within 30 days after the tax debt is fully paid. Processing and recording times may vary, so the release should be confirmed when a property transaction or other deadline is involved.

-

No. Currently Not Collectible status may temporarily stop most active collection activity because of financial hardship, but it does not eliminate the debt or automatically remove a Notice of Federal Tax Lien. Penalties and interest generally continue.

-

Missing tax returns can limit available resolution options. The IRS generally requires filing compliance before approving many payment arrangements or considering an Offer in Compromise. Filing the correct returns may also change the amount owed if the IRS previously prepared substitute returns.

-

An authorized tax professional can communicate with the IRS, review transcripts, prepare Form 12153, present collection alternatives, and represent the taxpayer during the appeal process. The representative should review the notice and deadline before taking action.