Form 2848 vs Form 8821: IRS Power of Attorney vs Tax Information Authorization

IRS Power of Attorney vs IRS Tax Information Authorization

If you have ever wondered, “Form 2848 vs Form 8821, which one do I actually need?” you are not alone. Many taxpayers, and even some professionals, mix up the IRS power of attorney form and the IRS tax information authorization form.

This guide gives you the real world difference between Form 2848 and Form 8821. You will see when each form is appropriate and how I decide which one to use in active IRS cases.

TLDR;

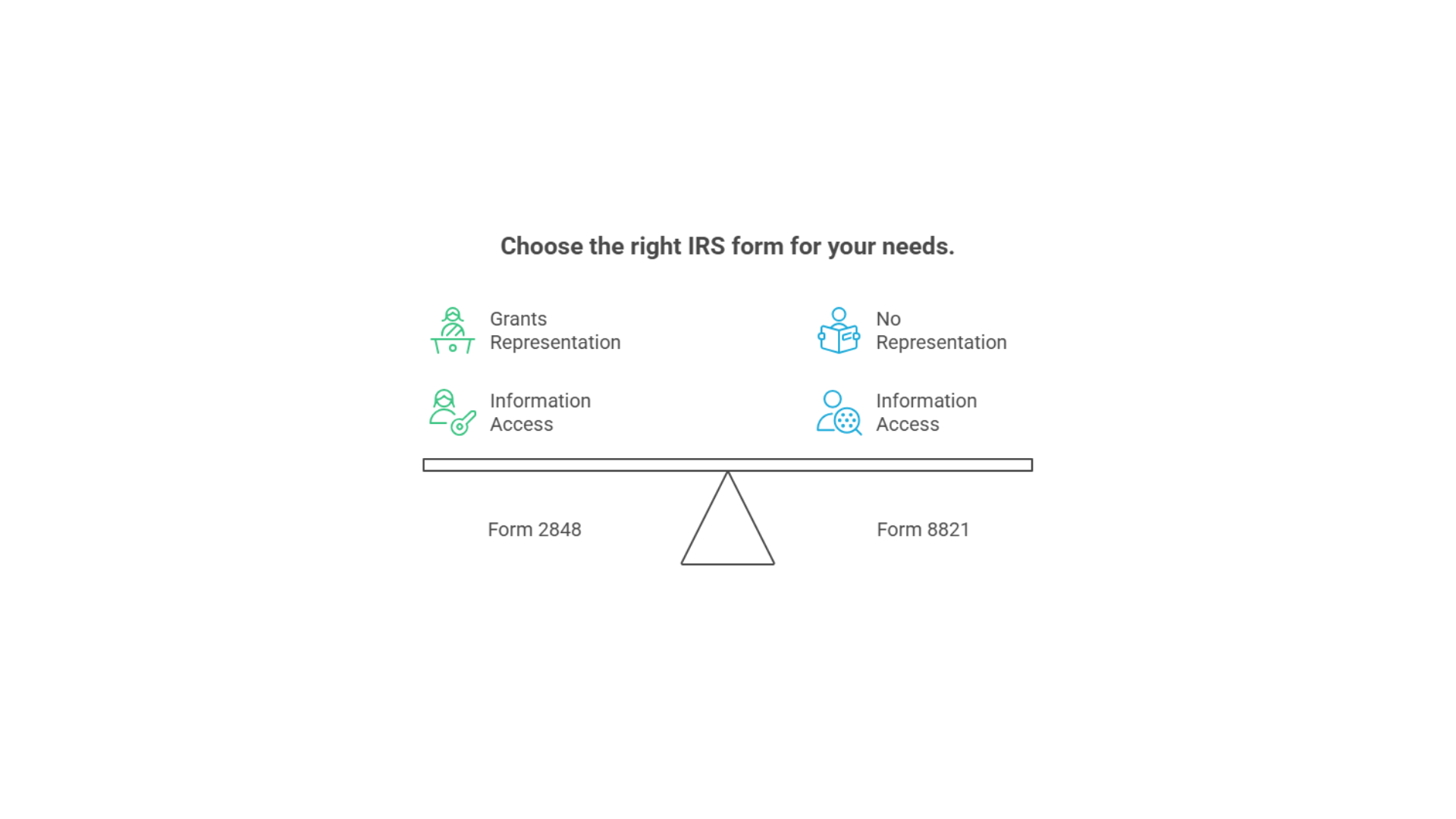

Form 2848 is for representation plus information access, it lets a qualified pro speak to the IRS and handle your case.

Form 8821 is for information access only, it allows transcripts and notices, but no representation and no IRS calls on your behalf.

Use 8821 for early diagnosis, transcript pulls, compliance review, and ongoing monitoring after resolution.

Use 2848 for active IRS matters, audits, collections, payment plans, OIC, appeals, lien and levy issues.

Who you name matters, 2848 is limited to IRS eligible reps like EA, CPA, attorney, while 8821 can be almost anyone or any organization.

2848 carries more responsibility and authority, 8821 is lighter scope and lower risk.

Both can be revoked or replaced, and reps can withdraw, cleaning up old authorizations prevents future problems.

Quick Answer, Difference Between Form 2848 and Form 8821

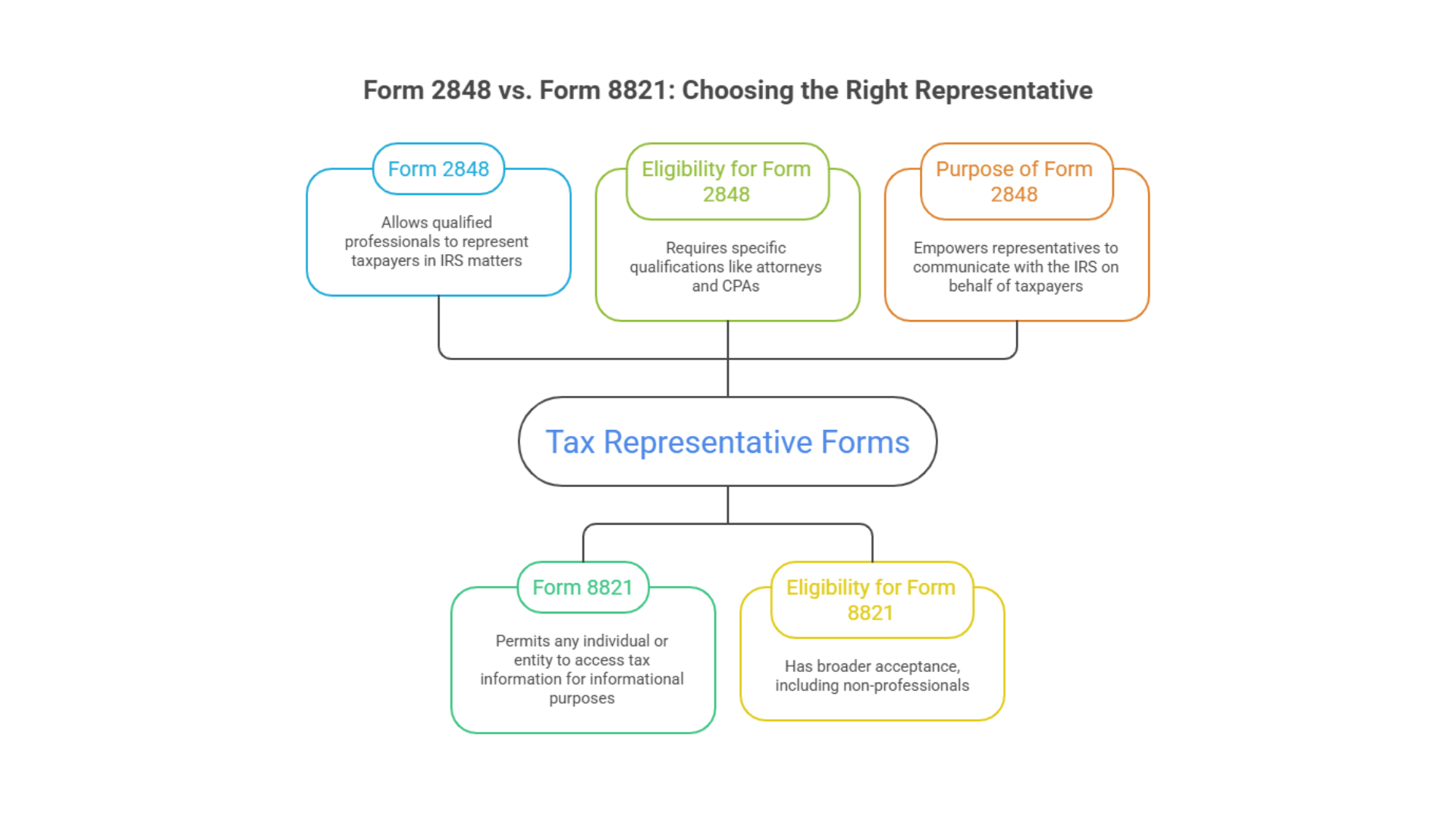

Form 2848, Power of Attorney and Declaration of Representative

This is the IRS power of attorney form. You use it when you want a qualified individual, such as an EA, CPA, or attorney, to represent you before the IRS. They can speak for you, attend conferences, and handle many tax matters for you.

Form 8821, Tax Information Authorization

This is the tax information authorization form. You use it when you want someone to inspect or receive your confidential IRS information, but not represent you.

Core Difference

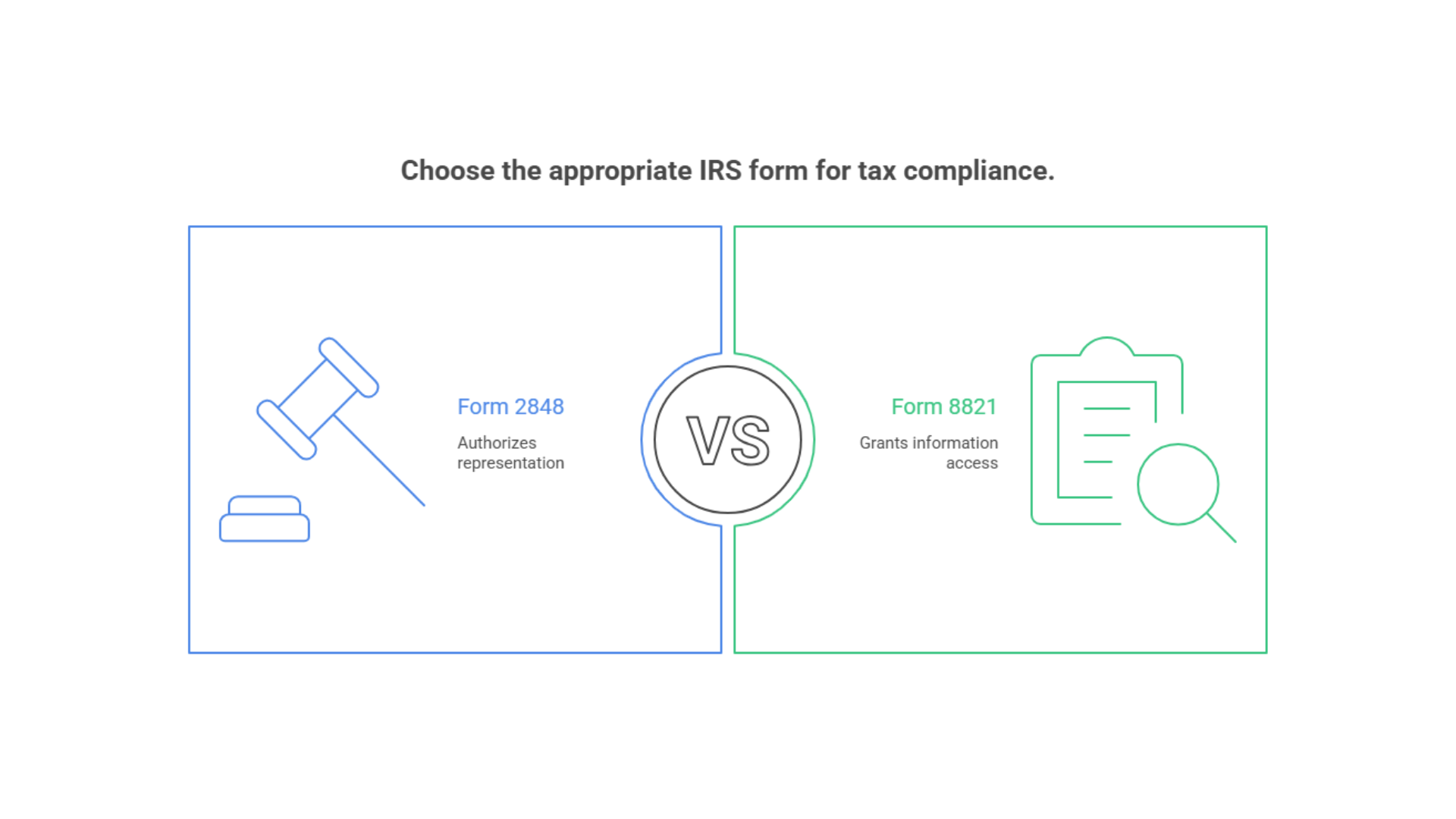

Form 2848 gives representation and information access.

Form 8821 gives information access only.

If you want a professional to speak to the IRS, negotiate IRS payment plans, stop collections, or appear on your behalf, you need Form 2848. If you only want someone to pull your IRS transcripts or review your records, Form 8821 is usually enough.

How I Decide Between Form 2848 vs Form 8821

When a new client comes in with tax debt, notices, or unfiled tax returns, I look at three things:

1. What stage are we in?

Early diagnosis, I start with Form 8821 so I can pull IRS transcripts and perform a clean review.

Active dispute or collections, I use Form 2848 so I can speak to the IRS directly and negotiate.

2. What job does the client actually need?

“Can you take over the IRS calls?”, this requires Form 2848.

“Can you look at my IRS account and tell me what is going on?”, this requires Form 8821.

3. Who needs access?

Bookkeeper or CFO, Form 8821 is perfect because they do not represent the taxpayer.

EA, CPA, or attorney handling an audit or settlement, that requires Form 2848.

4. Risk and responsibility

Form 2848 carries significant responsibility. The IRS treats this as formal representation. Form 8821 is only for information access.

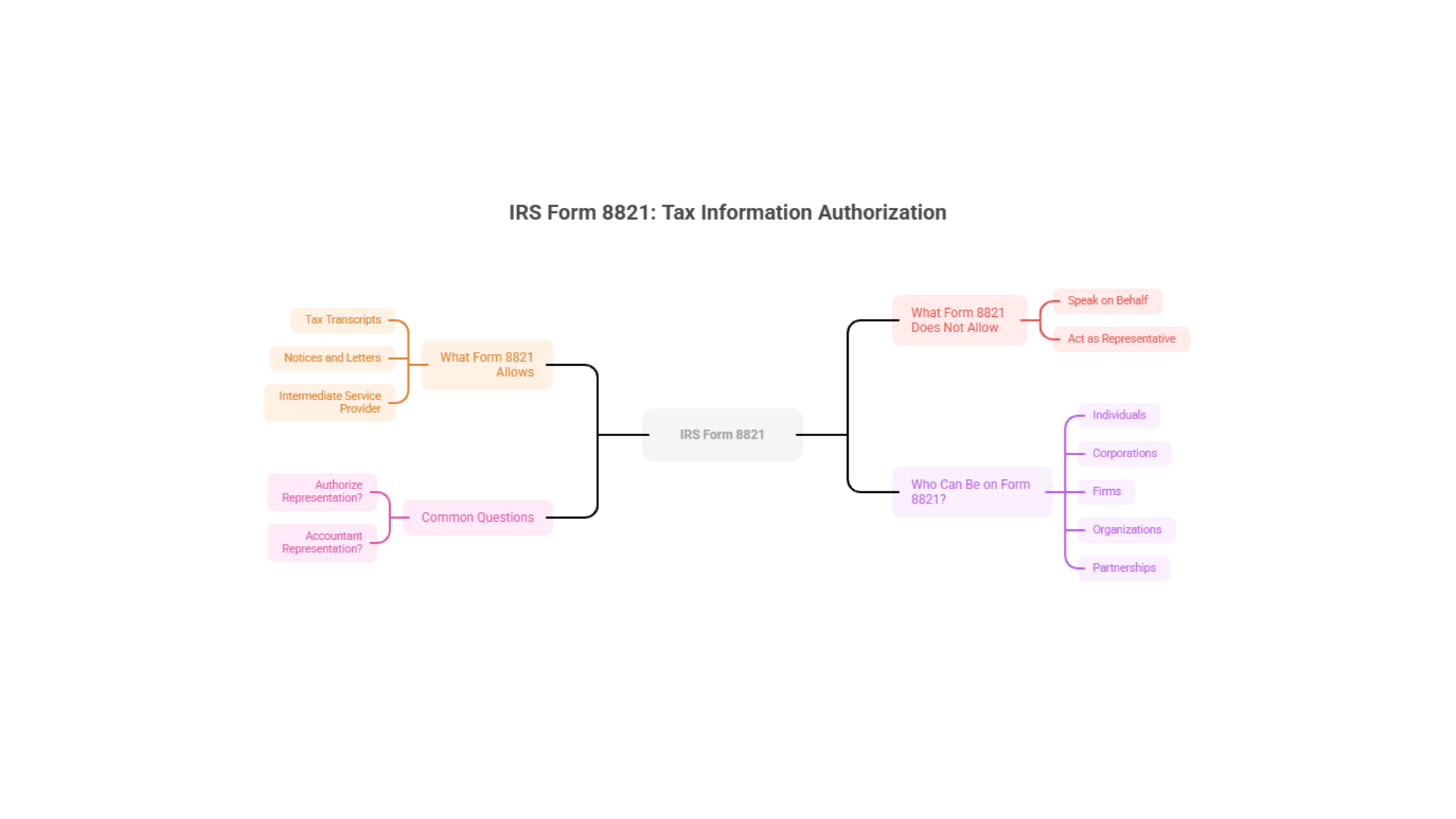

Deep Dive: What IRS Form 8821 (Tax Information Authorization) Really Does?

The IRS describes Form 8821 as a way to let another party inspect and receive your confidential tax information for the types of tax and periods you list on the form.

What Form 8821 allows

Access to tax transcripts, including account transcripts, wage and income transcripts, and return transcripts for the listed years.

Copies of notices and letters for the tax matters listed.

The ability to use an intermediate service provider, such as certain IRS transcript tools, when the box is checked.

This is why using Form 8821 for transcript access and tax review is standard practice among tax pros.

What Form 8821 does not allow

The IRS is very clear in the instructions. Form 8821 does not authorize your designee to speak on your behalf or act as your representative.

Common questions

Can Form 8821 authorize representation with the IRS?

No. It is information only.

Can my accountant use Form 8821 to represent me?

No. They can receive information, but they cannot represent you based on Form 8821 alone.

Who can be on Form 8821?

Per the IRS instructions, you can name any individual, corporation, firm, organization, or partnership to receive your information.

This is why Form 8821 is often used for:

Bookkeepers

CFOs or internal finance staff

Loan officers or advisors needing IRS proof

Other tax professionals assisting in an information gathering role

Deep Dive: What IRS Form 2848 (Power of Attorney and Declaration of Representative) Really Does?

IRS Form 2848 is the official IRS representative form. The IRS states that you use Form 2848 to authorize an individual to represent you before the IRS.

What Form 2848 allows

With a valid Form 2848, the representative can:

Talk directly to the IRS on your behalf about the tax matters and years listed.

Receive and review your confidential information.

Appear at IRS conferences and hearings.

Sign certain agreements and consents related to assessments, extensions, or adjustments within the scope of the POA.

This is why using Form 2848 for IRS payment plans, tax settlements, audits, and Offers in Compromise is standard in a tax relief practice.

Who can sign Form 2848 vs Form 8821 as the representative

For Form 2848, the IRS is strict. Your representative must be eligible to practice before the IRS, such as:

Attorney

Certified Public Accountant

Enrolled Agent

Enrolled actuary

Certain enrolled retirement plan agents

Certain law or accounting students under special authorization

So for “who can sign Form 2848 vs Form 8821”:

2848, limited to the qualified categories listed above.

8821, much broader, any individual or entity for information only.

Does Form 2848 allow my tax pro to talk to the IRS for me?

Yes. That is the entire purpose of Form 2848. If you are searching “IRS Form 2848 tax attorney near me,” you are looking for someone who can be that voice with documented authority.

When to Use Form 2848 vs Form 8821, Practical Scenarios

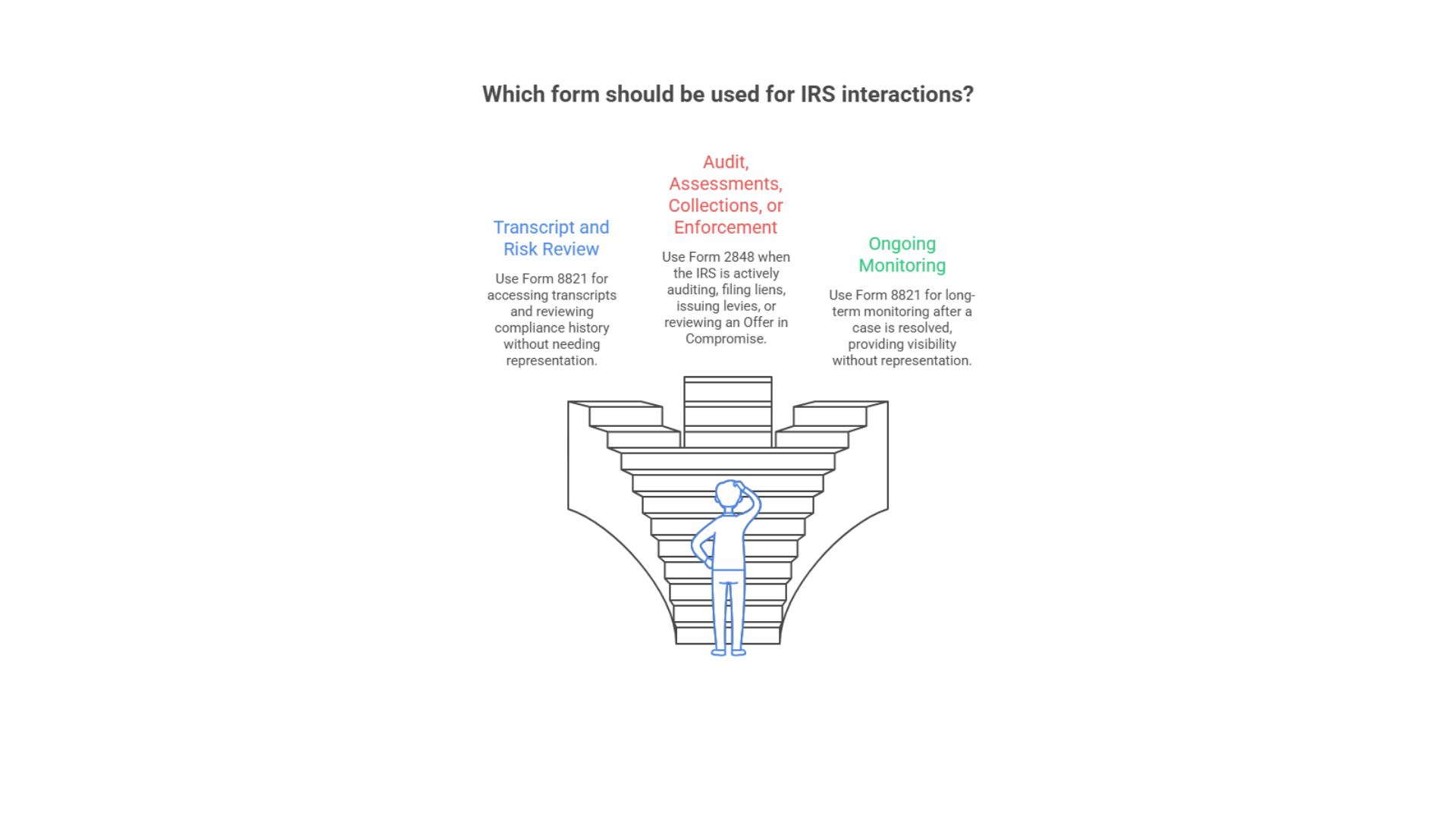

1. Transcript and risk review only

I start with Form 8821 so I can pull transcripts and review compliance history.

2. Audit, assessments, collections, or enforcement

When the IRS is auditing, filing liens, issuing levies, or reviewing an OIC, I use Form 2848.

3. Ongoing monitoring after a resolved case

For long term monitoring, Form 8821 is perfect because you only need visibility, not representation.

How to Fill Out IRS Form 2848 Power of Attorney, High Level Checklist

This is not a line by line walkthrough. The IRS already provides detailed IRS Form 2848 instructions for taxpayers with tax debt. Here is how I explain it to clients.

Key parts you will see on Form 2848

Taxpayer information, Part I line 1

Your name, address, TIN, and phone number.

Representative information, Part I line 2

Your Enrolled Agent, CPA, or attorney details, including their CAF number and contact information.

Tax matters, Part I line 3

The type of tax, such as income or employment.

The form numbers, such as 1040, 941, 940, 1120.

The specific tax years or periods.

Acts authorized and limitations

The form and instructions explain what your representative can do and any restrictions you want to place.

Signatures and dates

You sign and date as the taxpayer.

Your representative signs the declaration of representative confirming their eligibility.

If you have tax debt, it is smart to read at least the summary portions of the IRS Form 2848 instructions or talk with a professional before listing tax periods so you do not leave out key years.

How Long These Forms Last

The IRS will keep the authorization on file for 7 years. Or until the taxpayer revokes them or a newer authorization replaces them. In addition, the Tax Professional may submit a withdrawal. I review and clean up old authorizations for every new client.

Revoking or Withdrawing Form 2848 or Form 8821

To revoke authorization, write “REVOKE” at the top of the form, sign, and send it to the IRS. To withdraw as a representative, write “WITHDRAW”, sign, and send it in. Many taxpayers forget to do this when they change tax professionals, which can cause problems later.

Final Checklist, Form 2848 vs Form 8821

You need Form 2848 if

You want a licensed pro to speak to the IRS

You are in an audit or collections

You need payment plans, levy releases, appeals, or settlements

You need Form 8821 if

You only want a professional to review your IRS information

You want ongoing transcript monitoring

You are still deciding next steps

If you are staring at an IRS notice and unsure which form to sign, consult with a qualified tax professional who handles IRS cases every day. This is the work my team and I do all week.